The Economics and Statistics Division maintains archives of previous publications for accountability purposes, but makes no updates to keep these documents current with the latest data revisions from Statistics Canada. As a result, information in older documents may not be accurate. Please exercise caution when referring to older documents. For the latest information and historical data, please contact the individual listed to the right.

<--- Return to Archive

For additional information relating to this article, please contact:

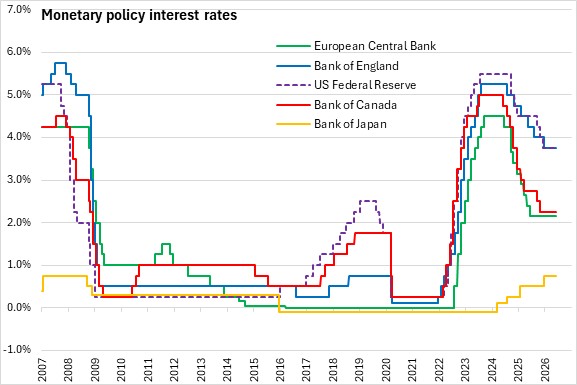

June 10, 2026BANK OF CANADA MONETARY POLICY The Bank of Canada maintained its target for the overnight rate at 2.25%, with the Bank rate at 2.50% and the deposit rate at 2.20%.

The conflict in the Middle East is still ongoing resulting in rise in energy prices and disruptions in global supply chain, which drive up inflation. US administration continues to propose new tariffs and trade policy uncertainty remains elevated.

US economic growth remains strong supported by consumption and AI-related investment. High energy prices have slowed economic growth in the Euro Area while exports are supporting economic growth in China.

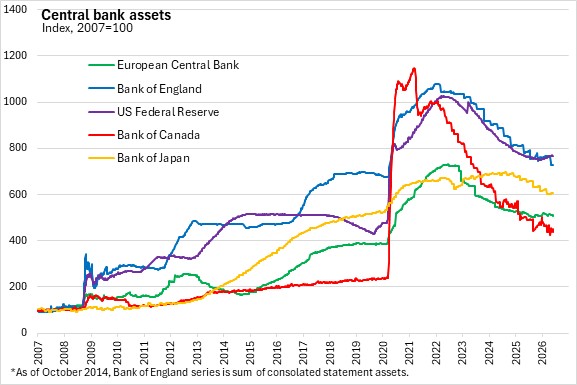

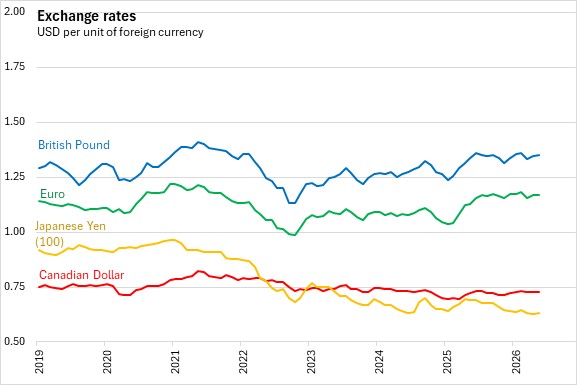

Canadian financial conditions have loosened further since the April Monetary Policy Report. Equity markets globally have stayed firm, bond yields have shown ongoing volatility, and the Canadian dollar has depreciated against the US dollar and other currencies.

In Canada, GDP edged down by 0.1% in Q1 2026, weaker than expected in the April MPR. Consumer spending grew 1.4% but government spending declined. Housing activity also declined and business investment remained weak. Exports fell while imports rose strongly as inventories were rebuilt. The Bank committee expects economic growth to rebound in the second quarter supported by consumption and housing but remain in excess supply.

Employment was up in May, and the unemployment rate continues to fluctuate in the 6 ½%-7%.

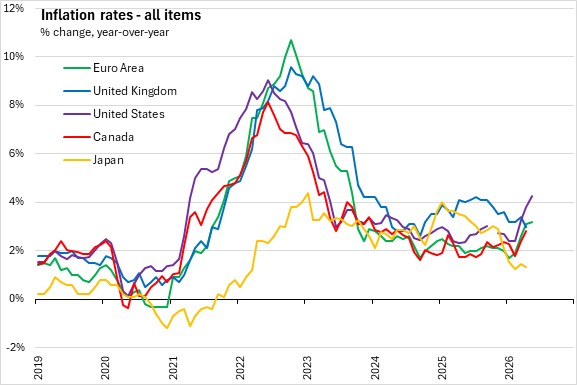

CPI inflation rose in April, reaching 2.8% which reflects high energy prices. Measures of core inflation have moved down to around 2%. Food price inflation moderated but remained high, and shelter inflation continued to slow. Total inflation is expected to be around 3% in the near term before easing gradually towards 2% based on elevated oil prices.

The Governing Council sees the current policy rate at about the right level to keep inflation close to 2.0% while closely monitoring the impact of the conflict in the Middle East and trade policy uncertainty. If the outlook changes, they are prepared to respond and will be assessing incoming data carefully relative to the Bank’s forecast.

The next scheduled date for announcing the overnight rate target is July 15, 2026 and the Bank’s next Monetary Policy Report will be released at the same time.

Source: Monetary Policy press release; Monetary Policy press conference

<--- Return to Archive