The Economics and Statistics Division maintains archives of previous publications for accountability purposes, but makes no updates to keep these documents current with the latest data revisions from Statistics Canada. As a result, information in older documents may not be accurate. Please exercise caution when referring to older documents. For the latest information and historical data, please contact the individual listed to the right.

<--- Return to Archive

For additional information relating to this article, please contact:

April 15, 2020BANK OF CANADA MONETARY POLICY Today, the Bank of Canada maintained the target for overnight rate at 0.25 percentage points, which the Bank of Canada considers this the effective lower bound. The Bank Rate (0.50 per cent) and the Deposit rate (0.25 percentage points) also remain unchanged.

The Bank of Canada’s recent actions in response to the economic shock from COVID-19 included lowering the target for the overnight rate 150 basis points and conducting lending operations to financial institutions and asset purchases in core funding markets of around $200 billion. These actions have eased market dysfunction and kept credit channels open.

The Bank of Canada views that the next challenge for markets will be managing increased demand by governments, business and households for near-term financing. The Bank of Canada believes the situation calls for special actions by the central bank and is taking several steps.

There was a previously announced program to purchase at least $5 billion per week in Government of Canada securities on secondary markets. The Bank will increase these purchases as required to maintain proper functioning of the government bond market.

The Bank is temporarily increasing the amount of Treasury Bills it acquires at auctions up to 40 per cent.

Today, a new Provincial Bond Purchase Program of up to $50 billion will supplement the previously-announced Provincial Money Market Purchase Program. In addition, under, a new Corporate Bond Purchase Program the Bank of Canada will acquire up to $10 billion in investment grade corporate bonds in the secondary market. The term repo facility will permit funding for up to 24 months.

The Bank of Canada did not publish their usual economic forecast, noting that the outlook is too uncertain at this point to provide a complete forecast. Analysis of scenarios suggests that real activity was down 1-3 per cent in Q1 2020 and will be 15-30 per cent lower in Q2 compared to Q4 2019. CPI inflation expected to be close to 0 per cent in Q2 2020 due to effects of lower gasoline prices. The Bank of Canada notes that Canadians will see increases in prices for some items given supply-side constraints and the weaker Canadian dollar. The following is a summary of the Monetary Policy Report which examines critical developments and recovery scenarios.

The Bank of Canada noted the suddenness of COVID-19 effects that created shockwaves in financial markets, including flight to safety, repricing of risky assets, and a breakdown in functioning of many markets. The fall in commodity prices, particularly oil, also weighs significantly on the Canadian economy. The global and Canadian economies are expected to rebound once the medical emergency ends but the timing and strength of economic recovery will depend on how the pandemic unfolds, on containment measures, and on changes in household and business behaviour.

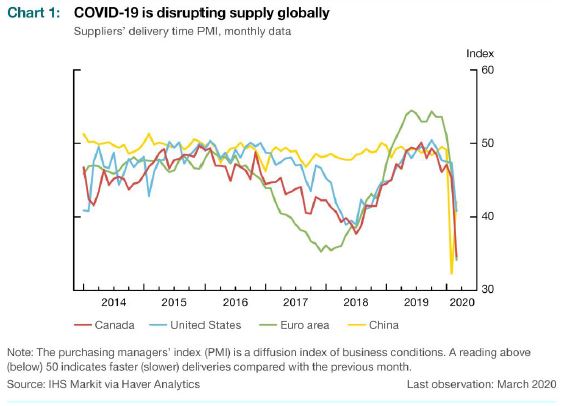

Global economic growth was stabilizing prior to the outbreak with the US-China trade agreement and strong labour markets. The sudden closure of many businesses and sharp declines in trade have disrupted global supply chains. This resulted in unemployment, lower incomes, elevated debt levels, and a hit to confidence that will weigh heavily on a range of economic activities. The global economy is expected to have a sharp contraction in the first half of 2020.

Countries will experience the impact and recover at different points of time, suggesting that the global recovery will be gradual. In China, the spread of the virus slowed by early March due to strict control measures that have been partially eased. Activity is expected to partially rebound once control measures are relaxed, but full recovery will take time. It is expected that businesses will restart in stages and gradually people will return to work. Lost income and the shock to confidence are anticipated to slow recovery process. Within the goods-producing sector, production will operate below capacity for some time due to supply chain disruptions and global trade is expected to remain weak until COVID-19 under control around the world. Rebounds in travel, tourism and entertainment could be tempered by ongoing concerns.

China’s re-opening is a possible case study for recovery in other regions. China’s industrial production and weekday travel are recovering but households are cautious about weekend movements.

Global financial systems are under stress. Volatility spiked to very high levels. Equity prices declined sharply. Market functions were impaired, with widening corporate and emerging-market credit spreads. There have been outflows from equities, emerging-market assets and corporate bonds. Credit tightening has been particularly pronounced in North American energy sector with the decline oil prices. The Bank of Canada notes that tight credit conditions could hamper recovery for highly indebted business and vulnerable emerging-market economies even after pandemic is under control. Amid the flight to safe assets, US government bond yields have fallen and the US dollar has appreciated against other currencies, including the Canadian dollar. Central banks have taken unprecedented actions to increase liquidity and maintain credit flows.

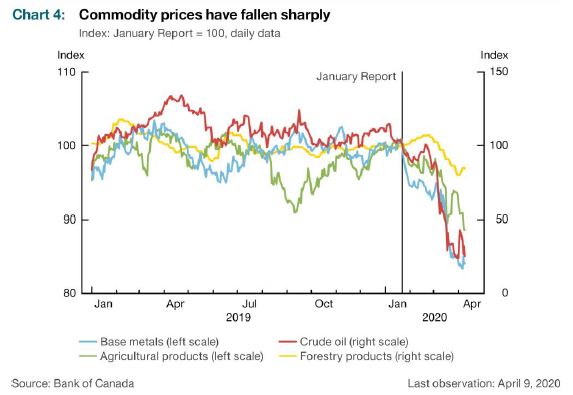

Commodity prices have fallen. The largest declines are for energy but there have also been significant declines across base metals, forestry, and agriculture products. Global crude oil prices have fallen 50-60 per cent since mid-January on expected lower demand from COVID-19 crisis and secondarily supply increase from major oil producers as they fight for market share in shrinking market. OPEC and some non-OPEC producers reached an agreement to reduce supply by 10 million barrels per day in May and June. The Bank of Canada notes that oil prices should increase when global economic activity normalizes but uncertainty is high due to elevated inventories, air transportation recovery, and supply agreements.

The Canadian economy was on solid footing but had notable challenges prior to the crisis in terms of household debt and the energy-sector. There are two new significant shocks to economy. First, COVID-19 pandemic and measures to control spread will dramatically impact activity and employment for a period of time. Uncertainty about the duration and severity of outbreak is affecting spending decisions by both household and business. Depressed foreign activity weighs on exports and investment while terms of trade weakened with lower commodity prices. Second, the decline in global oil prices is major setback to the energy sector and production and investment have declined sharply and are likely to remain low.

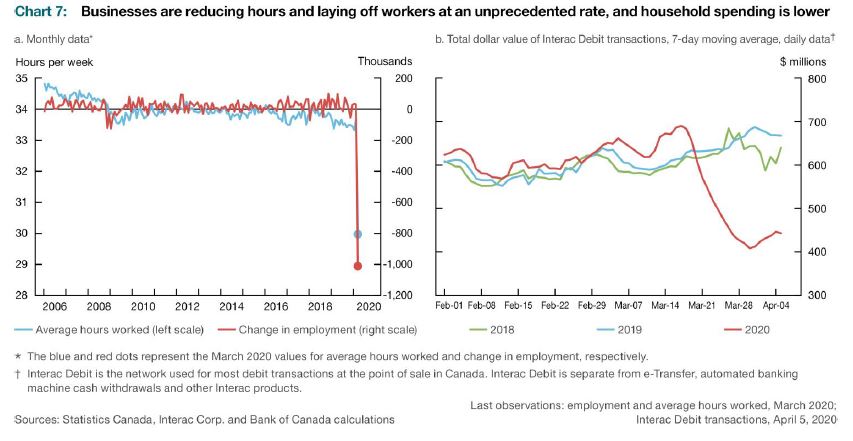

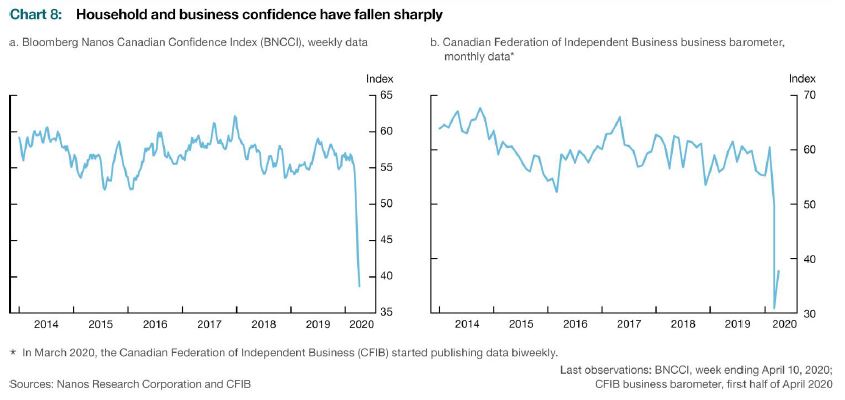

Businesses have reduced hours, laid off workers and reduced investment. This is expected to trigger declining household income and spending that reinforce the declining business activity. In March, more than one million jobs were lost and over two million workers reported fewer than typical hours or no hours. Household wealth has decreased with the decline in the stock market and is likely to have consumers increasing precautionary savings and restraining discretionary spending. Financial institutions have introduced programs to provide flexibility and payment deferrals on mortgages, credit cards and lines of credit.

Various fiscal, monetary and financial policy measures have been implemented to help offset income loses, increase credit access, and lower debt servicing costs. The Bank of Canada notes that the fiscal policy been designed to adjusted to size of impact on employment and activity.

The Bank of Canada believes the economy will recover as businesses reopen and people start returning to their normal lives. Recovery will be supported through several channels. As control measures ease, non-essential businesses will reopen and recall workers at brisk pace. The government’s wage subsidy will support this by keeping a link between workers and employers, so that job matching is faster and less costly. Fiscal policy support should help prevent long-lasting declines in confidence, however, output is likely to remain below pre-pandemic levels for some time. Business confidence is expected to strengthen as demand picks up and consumer spending should rebound with some pent-up demand after the current period of restraint. The housing market will benefit from rebound in household income and low borrowing costs. Although oil prices are expected to remain low, recovery in foreign demand and a weaker Canadian dollar will support non-commodity exports.

The economy may see positive innovations in the way services are delivered and work is organized – an acceleration of ongoing structural changes. Longer term benefits could also emerge from online sales and the digital economy as consumers permanently adopt the tools used to minimize disruptions. Teleworking could reduce geographic barriers to workers, improving flexibility and dynamics of the labour market.

The Bank of Canada notes that Canada’s financial system, tested through top-down stress-testing exercises, is resilient and large lenders are positioned to weather a severe economic and financial downturn.

With the outlook for economic activity highly uncertainty, the Bank developed a set of scenarios for consideration.

In the Bank’s first scenario, containment measures are relaxed soon, and policy measures limit any structural damage in Canada or major trading partners. Foreign demand resumes and global supply chains are return to operation in relatively short-order. Consumers and business confidence levels recover. Most of the affected industries tend to have higher job turnover, employing younger more mobile workers, which helps limit skill mismatches and search costs during recovery. There would be rapid recession followed by strong rebound.

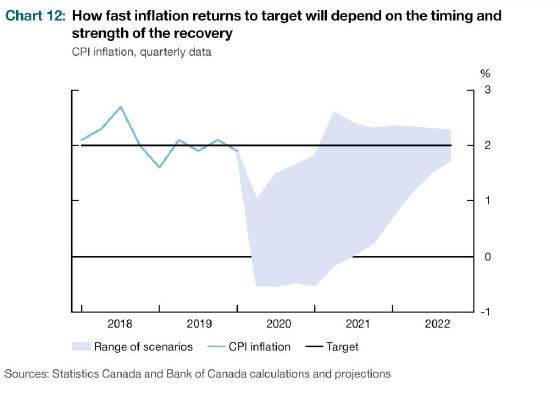

The second scenario considers a more severe impact on households and businesses. A longer period of control measures leads to significant number of permanent business closures and bankruptcies. The productive value of plant, equipment, and human-knowledge for some firms would be lost. As an example, lost exporters during the 2008-09 recession weighed on export recovery. In this scenario, workers would need to relocate and be employed in different industries, prolonging unemployment and increasing skill erosion. This type of structural damage could be permanent or take years to be undone. The recovery of foreign demand in this scenario is slower and oil prices remain weak leading to further business shutdowns and contracting activity. The prolonged downturn leads to higher debts for households, businesses and governments when the recovery begins. Weaker balance sheets lead to slower growth going forward. Under this scenario, economic activity would remain below pre-pandemic levels for extended period – beyond the end of 2022 (see chart).

Under either scenario, the weak economic outlook slow inflation but there is considerable uncertainty about prices. Determining future inflation is difficult with both supply and demand falling. Short-term inflation is expected to be close to 0 per cent with lower gasoline prices and tourism related prices. Higher import prices from the lower Canadian dollar will put upward pressure on prices. Under the more favourable scenario, inflation quickly returns to target as previous oil price decline dissipates and excess supply is quickly reabsorbed. The Bank of Canada notes that current environment is more uncertain for the inflation outlook and views downside risks as larger. There is a possibility that cautious consumers could impair recovery in certain sectors like travel/restaurants or keep demand weak. Upside risks exists if demand rebounds faster than supply and gets support from pent-up demand as well as the substantial fiscal and monetary stimulus in place. Supply chain and labour market disruptions, i.e. fewer temporary foreign workers, could led to upward price pressures for specific goods and services.

Technical challenges to measuring inflation during this period may also occur. With CPI inflation measured using fixed weights, substantial changes in consumer spending patterns will not be captured. Increased demand for medical products and food in stores could lead to larger price increases while declining pries for energy and flights are given weights based on previous consumption patterns. The Bank of Canada see that its core inflation measures will be helpful to look beyond some of this volatility.

Bank of Canada: Rate announcement, Monetary Policy Report – April 2020

The Bank of Canada's next scheduled date for announcing the overnight rate target is June 3, 2020. The next full update of the Bank’s outlook for the economy and inflation, including risks to the projection, will be published in the MPR on July 15, 2020

<--- Return to Archive