For additional information relating to this article, please contact:

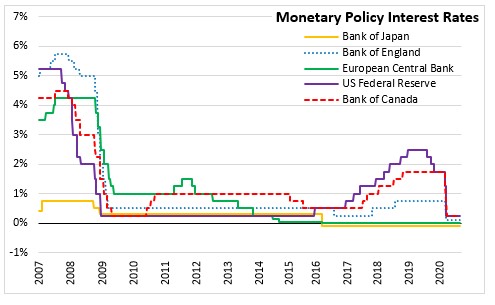

October 29, 2020BANK OF JAPAN MONETARY POLICY The Policy Board of the Bank of Japan decided to maintain the negative interest rate of -0.1 per cent on balances of financial institutions at the Bank. The Bank of Japan will also purchase a necessary amount of Japanese government bonds (JGBs) without setting an upper limit in order to keep the 10-year JGB yields at around zero per cent. However, yields may move up or down depending on economic activity and prices.

In addition, the Bank will actively purchase exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs) so that their amounts outstanding will increase at annual paces with upper limit of about 12 trillion yen and about 180 trillion yen, respectively. Commercial paper (2.0 trillion yen) and corporate bond (3.0 trillion yen) holdings by the Bank will be maintained. The Bank will make additional purchases with the upper limit of the amounts outstanding of 7.5 trillion yen for each asset until the end of March 2021.

The Bank will continue with "Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control," aiming to achieve the price stability target of 2 per cent, as long as it is necessary for maintaining that target in a stable manner. It will continue expanding the monetary base until the year-on-year rate of increase in the observed CPI (all items less fresh food) exceeds 2 per cent and stays above the target in a stable manner.

In response to COVID-19, the Bank will continue to support financing of firms and maintain financial market stability through:

- the Special Program to Support Corporate Financing,

- provision of yen and foreign currency funds without setting upper limits, and

- active purchases of ETFs and J-REITs.

Japan’s economy has picked up with the easing of containment measures. However, the pace of economic recovery is expected to be only moderate as economic around world react to the evolution of the pandemic carefully. With improved conditions in global demand, exports and industrial production have been on an upward trend in Japan. Reflecting the continued impacts of the pandemic, employment and income levels have been weak while business fixed investment has been declining. While private consumption has started to gain momentum, consumption of services such as eating and drinking, and accommodations has remained at a low level. Public investment has continued to increase but financial conditions have been weak for corporate financing.

The year-over-year rate of the change in the consumer price index (CPI, all items less fresh food) is likely to be negative, mainly due to decline in crude oil prices, the “Go to Travel” campaign and the impacts of COVID-19. The annual inflation rate is expected to turn positive and increase gradually as the downward pressure on prices wane slowly as economic conditions improve.

Japan’s economy is expected to follow an improving trend supported by accommodative financial conditions and the government's economic measures. The pace of growth is expected to be moderate in the short-term and start improving further as global economies return to a steady growth path.

Compared with the previous projections in the July Outlook Report, the projected growth rate is lower for fiscal 2020, mainly due to a delay in recovery in services demand, but is somewhat higher for fiscal 2021 and more or less unchanged for fiscal 2022.The outlook continues to be very uncertain due to the risks of COVID-19 on domestic and global economic conditions.

The Bank noted that it will closely monitor the impacts of COVID-19 on the Japanese economy and is prepared to take additional easing measures as needed. The Bank expects short- and long-term policy interest rates to remain at their present or lower levels for the time being.

Source: Bank of Japan, Statement on Monetary Policy, Outlook for Economic Activity and Prices (October 2020)